Every year, millions of Canadians rush to file their taxes before the deadline.

Receipts get pulled out of drawers, spreadsheets get updated at the last minute, and accountants work overtime trying to make sense of months or sometimes years of financial activity.

And by the time most people start thinking about their taxes, the financial decisions that determine their tax bill have already been made.

That means many Canadians end up paying more tax than they legally need to.

According to the Canada Revenue Agency (CRA), individuals and businesses are responsible for ensuring their tax filings are accurate and compliant with Canadian tax law.

However, the CRA also acknowledges that many taxpayers miss deductions, misreport expenses, or fail to plan effectively simply because they lack the right guidance throughout the year.

For many families and small business owners, taxes are treated like a once-a-year administrative task instead of what they actually are:

A financial strategy.

And when taxes are treated as an afterthought, people lose opportunities to:

- reduce their tax burden legally

- structure income properly

- plan major financial decisions

- protect their long-term wealth

This is why more Canadians, especially entrepreneurs, freelancers, and growing businesses, are moving toward a different approach to working with their accountant.

Instead of hiring an accountant only during tax season, they work with a professional throughout the year. This model is often called a tax membership, and it focuses on proactive tax planning in Canada rather than reactive tax filing.

The difference may seem small at first, but the financial impact can be significant.

In this article, we’ll explain:

- Why the traditional tax model often fails Canadians

- How a tax membership works

- And why year-round tax planning is becoming the smarter way to manage taxes in Canada

If you’ve ever wondered whether there’s a better way to approach your taxes, this guide will help you understand the options clearly.

The Traditional Tax Model (And Why It Fails)

For decades, the relationship between most Canadians and their accountant has followed the same pattern.

Taxes are ignored for most of the year, and then suddenly become urgent in March or April.

At that point, the process typically looks like this:

- Gather documents

- Send everything to an accountant

- Wait for the return to be prepared

- Sign and file before the CRA deadline

Technically, this system works. The tax return gets filed, and the requirement to report income to the CRA is fulfilled.

But there is a major limitation with this approach.

It focuses on tax filing, not tax planning.

That difference matters more than many people realize.

When an accountant only sees your finances once per year, they are looking at events that have already happened. The income has already been earned, the expenses have already been incurred, and the financial decisions that influence your taxes have already been made.

At that point, the accountant’s job is mostly administrative. They can make sure everything is accurate and compliant, but their ability to improve the outcome is limited. For example, consider a small business owner who only meets with their accountant during tax season. If that business owner could have saved tax by adjusting their compensation strategy, perhaps through a different mix of salary and dividends, that decision needed to be made months earlier.

The same applies to families making decisions about RRSP contributions, tax credits, or income splitting strategies. By the time the return is being prepared, many of those opportunities have already passed.

This is one of the reasons the CRA encourages taxpayers to understand their financial situation and plan ahead rather than waiting until filing season.

Another problem with the traditional model is that it often leads to disorganized financial records. When bookkeeping and documentation are handled only once per year, it becomes much harder to track expenses accurately or maintain clean records. This creates unnecessary stress during tax season and increases the risk of mistakes.

For business owners, it can also create deeper problems.

Without consistent financial oversight, owners may not have a clear picture of their cash flow, tax obligations, or profitability. Important business decisions end up being made without reliable financial data.

Over time, this reactive approach can quietly cost people money. Not because anyone is doing anything wrong, but because the system itself is designed around reporting the past instead of planning the future. This is exactly where the concept of a tax membership begins to change the conversation.

What is a Tax Membership?

To understand tax membership, it helps to think about the difference between emergency care and preventive care.

Emergency care solves a problem after it appears.

Preventive care focuses on avoiding the problem in the first place.

Traditional tax services are similar to emergency care. An accountant steps in once per year to prepare and file the return based on what has already happened.

A tax membership, on the other hand, focuses on ongoing tax planning in Canada throughout the year.

Instead of interacting with your accountant once annually, you have structured access to advice, guidance, and financial oversight during the year when decisions are actually being made.

This shift changes the role of the accountant entirely. Rather than simply preparing tax returns, the accountant becomes a financial guide who helps clients make smarter decisions about income, expenses, and business strategy.

A typical tax membership may include several components:

- Ongoing tax advice and planning

- regular reviews of financial activity

- support with bookkeeping or payroll

- guidance on major financial decisions

- preparation and filing of tax returns when the time comes

Because the relationship is ongoing, the accountant is able to spot opportunities that would otherwise be missed.

For example, a freelancer might receive advice on setting aside taxes properly or registering for GST/HST at the right time. A growing business owner might receive guidance on whether incorporation makes sense for their situation. A family might receive advice about maximizing tax credits or structuring their finances more efficiently.

In each case, the goal is not simply to prepare a return.

The goal is to help the client make better financial decisions before tax season arrives.

This approach aligns closely with the CRA’s broader guidance around financial responsibility and compliance. Planning ahead makes it easier to remain compliant with Canadian tax rules while also taking advantage of legitimate tax strategies available under the law.

For many Canadians, especially small business owners and self-employed professionals, the membership model offers something that the traditional tax model often cannot:

Clarity throughout the year.

Instead of scrambling to understand finances once a year, clients receive ongoing support that helps them stay organized, informed, and prepared.

And when tax season finally arrives, it becomes far less stressful because the real work of planning has already been done.

The Four Stages of Financial Complexity

One of the reasons taxes become confusing for many Canadians is that financial complexity grows over time. The tax strategy that works when you first start earning income is rarely the same strategy that works when you begin running a business or preparing for retirement.

In other words, tax planning in Canada is not one-size-fits-all. The level of planning required depends largely on the stage of life or business someone is in.

Most taxpayers move through four broad stages of financial complexity. Understanding these stages helps explain why a structured tax membership can make such a difference.

Stage 1: Individuals and Families Managing Personal Finances

At the first stage, the focus is usually on personal income and household finances. Many Canadians in this category are employees, parents, or professionals managing a family budget.

Their tax situation often revolves around things like employment income, childcare expenses, education credits, and retirement contributions such as RRSPs and TFSAs.

While these tax returns may appear straightforward, there are still important decisions that can affect how much tax someone pays. Families often benefit from strategies such as income splitting, careful timing of RRSP contributions, and claiming credits correctly. The CRA guides many of these deductions and credits here:

Without proper guidance, it’s surprisingly easy for families to miss these opportunities. That’s why even at this stage, proactive tax planning in Canada can make a noticeable difference.

Stage 2: Freelancers and Self-Employed Professionals

The next level of financial complexity often begins when someone starts earning income outside of traditional employment. Freelancers, contractors, and self-employed professionals suddenly have to deal with issues they may never have faced before.

Income may come from multiple clients instead of a single employer. Expenses must be tracked carefully. There may be obligations to register for GST/HST depending on revenue thresholds.

At this stage, proper small business tax planning becomes important. The way expenses are recorded, how income is structured, and whether bookkeeping is handled correctly can all influence the final tax outcome.

Many people at this stage start realizing that taxes are no longer just about filing a return. They begin to see the value of working with a tax accountant in Canada who can guide them through the decisions that arise throughout the year.

Stage 3: Incorporated Business Owners

When a business becomes incorporated, financial complexity increases again. Incorporation introduces a separate legal entity with its own tax obligations, which brings both opportunities and responsibilities.

Owners must think about issues such as:

- How to pay themselves (salary vs dividends)

- How corporate profits are retained or reinvested

- How corporate and personal taxes interact

This is where corporate tax planning in Canada becomes critical. The decisions made at this stage can influence both immediate tax costs and long-term wealth building.

Many incorporated business owners also begin thinking about retirement planning, shareholder structures, and how to manage profits in a tax-efficient way.

Without regular advice, these decisions can easily become overwhelming.

Stage 4: Growth-Stage Companies and Exit Planning

At the highest level of financial complexity are businesses that are focused on scaling, attracting investment, or preparing for a potential exit.

Here, the conversation shifts from simply managing taxes to building business value. Financial structure, operational systems, and strategic planning all start playing a role in the long-term worth of the company.

For founders in this stage, tax strategy in Canada becomes closely tied to succession planning, valuation, and wealth preservation.

Many entrepreneurs begin asking bigger questions:

How valuable is my business today?

What would a buyer see during due diligence?

How can I reduce tax exposure if I eventually sell?

Each stage builds on the previous one. As financial complexity grows, so does the need for thoughtful, year-round tax planning.

This is one of the reasons the traditional once-per-year tax model often struggles to keep up.

What Happens When You Don’t Plan Taxes Year-Round

Once you understand how financial complexity evolves, another question naturally follows.

What happens when people continue managing their taxes using the traditional once-per-year approach?

The answer is not always dramatic. In many cases, the consequences appear quietly over time rather than all at once.

1. Overpaying taxes.

Without ongoing tax planning in Canada, many individuals and business owners simply report income and expenses exactly as they appear. While this satisfies reporting requirements, it may ignore legitimate tax strategies that could reduce the overall tax burden.

For example, a business owner who never reviews their financial structure during the year might miss opportunities related to compensation planning or business deductions. Similarly, a family that waits until filing season may realize too late that certain tax credits or contributions could have been handled differently months earlier.

2. Disorganized financial records.

When bookkeeping and documentation are handled only once per year, information can easily be lost or forgotten. Receipts disappear, expenses become harder to categorize, and financial reports become less reliable.

This doesn’t just create stress during tax season. It can also make it difficult to make informed financial decisions during the year.

For business owners in particular, this lack of visibility can affect everything from hiring decisions to investment plans.

3. Increased risk during a CRA review or audit.

The Canada Revenue Agency expects taxpayers to maintain accurate records that support the information reported on their returns. Their guidance on record-keeping can be found here:

Without consistent financial oversight, taxpayers may find themselves scrambling to reconstruct records if questions arise.

None of these outcomes happen because people are careless. Most Canadians are simply busy managing their careers, families, and businesses. Taxes often fall to the bottom of the priority list until a deadline forces attention back to them.

But by the time that deadline arrives, the opportunity to influence the outcome has often passed.

This is where the concept of a tax membership begins to show its real value.

The Real Financial Benefit of Membership

When people first hear about a tax membership, the immediate question is often practical.

Is it worth it?

To answer that question, it helps to understand how traditional accounting services are typically structured.

Under the traditional model, services are often provided individually. A client may pay separately for tax preparation, bookkeeping assistance, business consulting, and financial advice.

Each service is delivered at different times, sometimes by different professionals, and often only when the client realizes they need help.

A tax membership, by contrast, brings these services together into an ongoing relationship.

Instead of interacting with an accountant only during tax season, clients receive continuous guidance throughout the year. This structure allows a tax professional to understand the client’s financial situation in greater depth and provide more timely advice.

The financial benefit comes from the ability to address issues earlier, when decisions can still influence the final outcome.

For example, consider a small business owner navigating small business tax planning in Canada. With regular guidance, they may receive advice about how to structure income, track expenses properly, and plan major financial moves in advance.

Those decisions can reduce tax exposure, improve financial organization, and create better long-term outcomes.

For incorporated businesses, the value may appear through more effective corporate tax planning Canada strategies, which can influence how profits are distributed or reinvested.

For families and individuals, the benefit often appears as greater clarity. Instead of feeling uncertain about taxes each year, they gain confidence that their financial decisions align with current Canadian tax rules.

The result is not simply a better tax return.

The result is a more informed financial life.

And when the next tax season arrives, it is no longer a period of confusion or urgency. Instead, it becomes a natural conclusion to a year of thoughtful planning.

That shift from reactive filing to proactive strategy is what makes the tax membership model increasingly appealing to Canadians who want more control over their finances.

Is a Tax Membership Right for You?

While the membership model offers clear advantages, it may not be necessary for every taxpayer. Some individuals have very simple financial situations that require only basic tax filing once per year.

However, for many Canadians, financial complexity increases gradually over time. Income sources expand, family responsibilities grow, and business activities become more sophisticated.

When that happens, the need for guidance often becomes more apparent.

A tax membership may be particularly helpful if you find yourself in one of the following situations:

- You run a business or earn self-employment income

- Your financial situation has become more complex over time

- You want proactive tax planning in Canada rather than reactive tax filing

- You would benefit from guidance on financial decisions during the year

- You prefer ongoing access to a tax accountant in Canada rather than a once-a-year interaction

For business owners, the value can be especially clear. Running a company involves constant financial decisions, from managing expenses and hiring staff to reinvesting profits or planning future growth.

In these cases, small business tax planning Canada becomes an ongoing process rather than an annual event. Similarly, incorporated companies often require thoughtful corporate tax planning Canada to ensure that compensation strategies, profit distributions, and long-term goals align with current tax regulations.

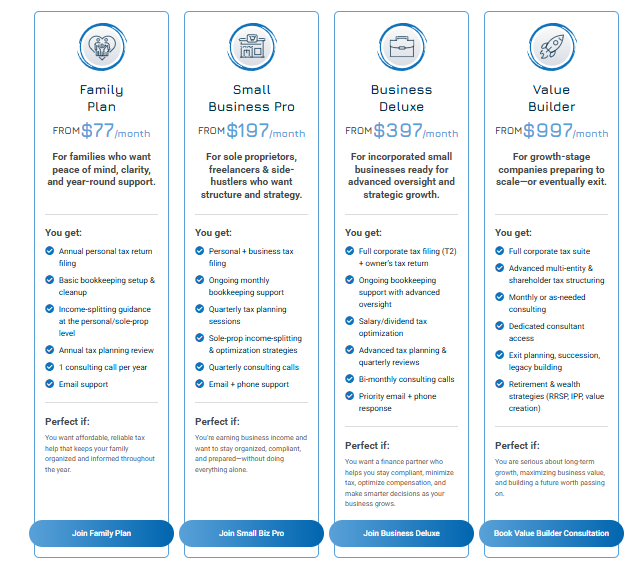

Bailey’s Tax Membership

Without guidance, making the right decision regarding proper tax planning given the level you are will feel overwhelming. But with the right support, they become part of a clear financial strategy.

At Bailey’s Tax Services Inc., we provide tax membership plans that guide you every step of the way from identifying what’s holding you back…to activating smart tax strategies…to finally achieving your goals with clarity and confidence.

Check out our membership plans here….

Conclusion

For decades, most Canadians have approached taxes the same way.

They wait until tax season arrives, gather their documents, and hope everything works out when the return is filed.

But as financial lives become more complex, that approach often falls short.

Taxes are not just a reporting requirement. They are a reflection of financial decisions made throughout the year. When those decisions are guided by thoughtful planning, the outcome can look very different.

A proactive approach to tax planning in Canada allows individuals and businesses to understand their financial position, identify opportunities earlier, and make decisions with greater confidence.

Instead of reacting to tax season, they prepare for it.

Instead of guessing, they plan.

And instead of seeing their accountant once per year, they build a working relationship that supports their long-term financial goals.

For Canadians who want greater clarity, better organization, and smarter financial decisions, the membership approach is simply a more modern way to manage taxes.

If you’re curious about how this model works in practice, you can explore the membership options offered by Bailey’s Tax Services here:

https://www.baileystaxservices.com/membership

Or, if you would prefer to speak directly with a professional about your situation, consider scheduling a consultation with a tax accountant in Canada who can help you evaluate your options.

Sometimes the most important financial step you can take is simply deciding to approach your taxes differently.

Meet Patrick

Patrick is a Tax Consultant, Educator, and Founder of Bailey’s Tax Services Inc, a tax advisory practice in Toronto, Ontario, Canada.

He specializes in helping Canadian families & small business owners who are stressed, confused, and overwhelmed about their financial state, understand their finances, make smart decisions that move them forward and attain clarity and peace of mind.

He regularly shares his knowledge and best advice here on his blog and on other channels such as LinkedIn and Facebook, and through his FREE monthly webinars (Teach Me For Free).

Book a call today to learn more about what Patrick and Bailey’s Tax Services Inc can do for you.